The global semiconductor market is experiencing a tectonic shift as industry priorities pivot from the mass consumer market toward AI infrastructure. While data centers are absorbing staggering volumes of memory, the personal electronics segment is grappling with spiraling costs. The third quarter is expected to bring a deceleration in price growth, yet systemic supply chain volatility will persist. The industry has reached a precarious tipping point, beyond which further price hikes could trigger a precipitous collapse in consumer demand.

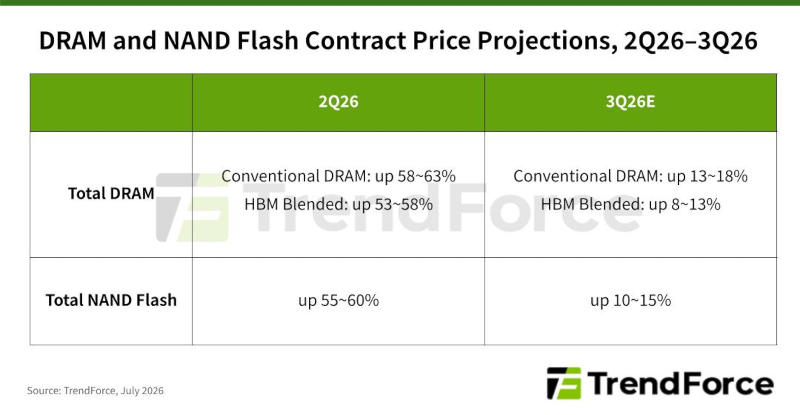

The DRAM market is transitioning into a phase of moderate expansion. Analytical data suggests that while supply constraints will persist through the third quarter, the growth rate of contract prices is expected to decelerate to between 13% and 18%. This slowdown is driven by two primary factors: the high base effect from previous periods and the gradual exhaustion of affordable demand within the consumer sector.

In the NAND flash segment, AI inference systems and the massive deployment of cloud infrastructure remain the primary catalysts. However, the outlook here is more precarious; prices have already hit record highs, and end-user tolerance for further increases has reached a breaking point. Consequently, the projected price growth for NAND in the reporting period is 10–15%, a significant drop compared to previous quarters.

The PC memory market is exhibiting distinct volatility. While laptop manufacturers continue to replenish their inventories, procuring components at inflated prices will inevitably drive up the retail cost of finished devices. This, in turn, could dampen overall shipment volumes by year-end. The DRAM shortage for PCs is further exacerbated by vendors reallocating production capacity toward the higher-margin server segment.

Server DRAM remains the bedrock for agentic AI workloads. The dominant platform continues to be general-purpose x86 servers utilizing RDIMM memory, prized for its high efficiency in multitasking environments. Forecasts indicate that demand for server hardware will remain robust through 2027. Improved CPU availability is expected to stimulate RDIMM consumption, particularly in the second half of 2026. Despite the ongoing shortage, price growth in this sector is expected to stabilize, thanks to long-term contracts that lock in supply costs.

The mobile segment finds itself in the most precarious position. Rising LPDRAM costs are forcing smartphone manufacturers to hike device prices, leading to a predictable contraction in sales. In response, brands are adopting more cautious procurement strategies. The paradox lies in the fact that chip suppliers continue to prioritize the AI segment, which sustains the LPDRAM shortage and pushes contract prices upward despite falling demand.

The outlook for graphics memory is mixed. The anticipated surge in demand for the GDDR7 standard—which was expected to trigger the release of professional solutions such as the Nvidia RTX PRO 6000 Blackwell—has failed to materialize. Furthermore, overall shipments of GDDR6 and GDDR7 have declined in tandem with the laptop market. Memory suppliers are swiftly redirecting capacity to other product lines, which is tightening the supply of graphics DRAM and sustaining the general upward price trend.

The traditional consumer electronics sector—specifically televisions and set-top boxes—remains weak. Relative stability is seen only in niche areas: automotive electronics, server SSDs, and networking equipment. Price growth in these segments is driven less by organic demand and more by strategic alignment among the market's largest players, coupled with the inability of Taiwanese brands to offset the deficit by scaling DDR4 production.

The consumer SSD market is currently locked in a protracted deadlock. OEM manufacturers accumulated significant inventories in the first half of the year and are now unwilling to accept further price hikes. This is forcing NAND suppliers to adopt more flexible strategies to prevent a total halt in shipments. Simultaneously, there is a clear pivot toward enterprise SSDs, fueled by the deployment of the Nvidia Vera Rubin platform. However, a shortage of internal DRAM continues to bottleneck the production of low-capacity, high-performance drives, maintaining the upward price trajectory.

The mobile storage segment (UFS and eMMC) is stabilizing. The primary refresh cycle for flagship models requiring the transition to the UFS 4.0 standard has concluded. Demand for mid- and low-end devices remains sluggish, leading to a relative expansion of supply. As OEMs are no longer willing to absorb rising costs, the pricing power of suppliers has waned, resulting in moderate contract price growth for eMMC and UFS.

Rounding out the landscape is the retail storage market—USB drives and memory cards—where demand remains stagnant. Module manufacturers are minimizing procurement, as high production costs cannot be fully passed on to the consumer. Suppliers continue to focus on high-margin AI and server products, limiting wafer allocation for the commodity market. Nevertheless, the general softening of demand for basic components will lead to a substantial slowdown in contract price growth during the third quarter.

The New Face of Samsung’s Wearable Intelligence

The New Face of Samsung’s Wearable Intelligence