The global AI arms race has decisively shifted toward the hardware layer. Stringent US sanctions and the ban on advanced Nvidia H200 accelerators have compelled Beijing to fast-track the development of its own silicon foundation. This transition is no longer merely a matter of political rhetoric; it has evolved into a massive reallocation of capital within China's largest corporations. This budgetary pivot toward domestic vendors signals the dawn of a new era for Asia's computing infrastructure.

Geopolitical tensions have acted as a potent catalyst for the Chinese semiconductor market. Restrictions on access to cutting-edge U.S. solutions have created a vacuum that domestic developments are now aggressively filling. According to data from Bloomberg Intelligence, Chinese companies intend to allocate up to 46% of their AI chip investments toward local manufacturers over the coming year—a radical surge compared to the current landscape, where domestic solutions account for barely 30% of expenditure.

The magnitude of this shift is underscored by a survey of executives from 60 of China's largest enterprises, spanning fintech, software development, retail, and heavy industry. Notably, 80% of respondents admitted to exceeding their initial infrastructure budgets. These overruns are driven not only by an escalating demand for raw computational power but also by the steep costs associated with migrating systems to non-Nvidia technology stacks.

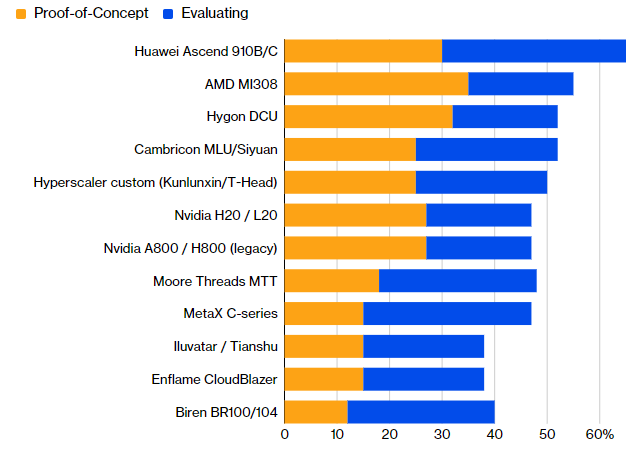

Within China's current computational landscape, a new hierarchy of influence has emerged. The undisputed frontrunner in terms of adoption and popularity is the Huawei Ascend 910B/C accelerator family. Huawei has successfully engineered a comprehensive ecosystem that, to a significant extent, challenges the long-standing dominance of Nvidia's CUDA. AMD's solutions, specifically the Instinct MI308, hold the second position, serving as a strategic "bridge" for companies not yet ready to commit to a full transition to local software.

The third spot is held by Hygon DCU chips, which are neck-and-neck with developments from Cambricon and specialized solutions from Alibaba’s Kunlunxin and T-Head. For Nvidia, the situation has become precarious: once the absolute industry standard, the company has now slipped toward the middle of the preference list. Even lesser-known players, such as Moore Threads and MetaX, are demonstrating stronger momentum in real-world infrastructure projects, largely due to the sheer accessibility of their hardware.

Beijing's strategic roadmap for the next five years is nothing short of ambitious, with planned investments in data center construction totaling $294 billion. This funding comes with a stringent mandate: at least 80% of high-tech components must be produced domestically.

However, the path to total autonomy is fraught with severe technological hurdles. The primary bottleneck remains the shortage of High Bandwidth Memory (HBM), without which modern Large Language Models (LLMs) suffer significant efficiency losses. Furthermore, the lithography limitations facing SMIC and other local foundries create a hard ceiling on chip performance. China currently faces a classic dilemma: architectural vision is outpacing manufacturing capacity, rendering the quest for technological sovereignty one of the most daunting engineering challenges of the decade.

The New Face of Samsung’s Wearable Intelligence

The New Face of Samsung’s Wearable Intelligence