The global AI arms race has evolved into a war of technological cycles, where a single disruption in the supply chain can trigger tectonic shifts across the market. Whispers of delays in the rollout of next-generation accelerators are enough to spark investor panic and cast doubt on the industry leader's hegemony. Recent reports suggesting postponed timelines for the Rubin Ultra and Kyber platforms represent the latest attempt to challenge the velocity of NVIDIA's innovation cycle. Yet, the swift response from the Santa Clara giant demonstrates that the actual pace of development far outstrips speculative projections.

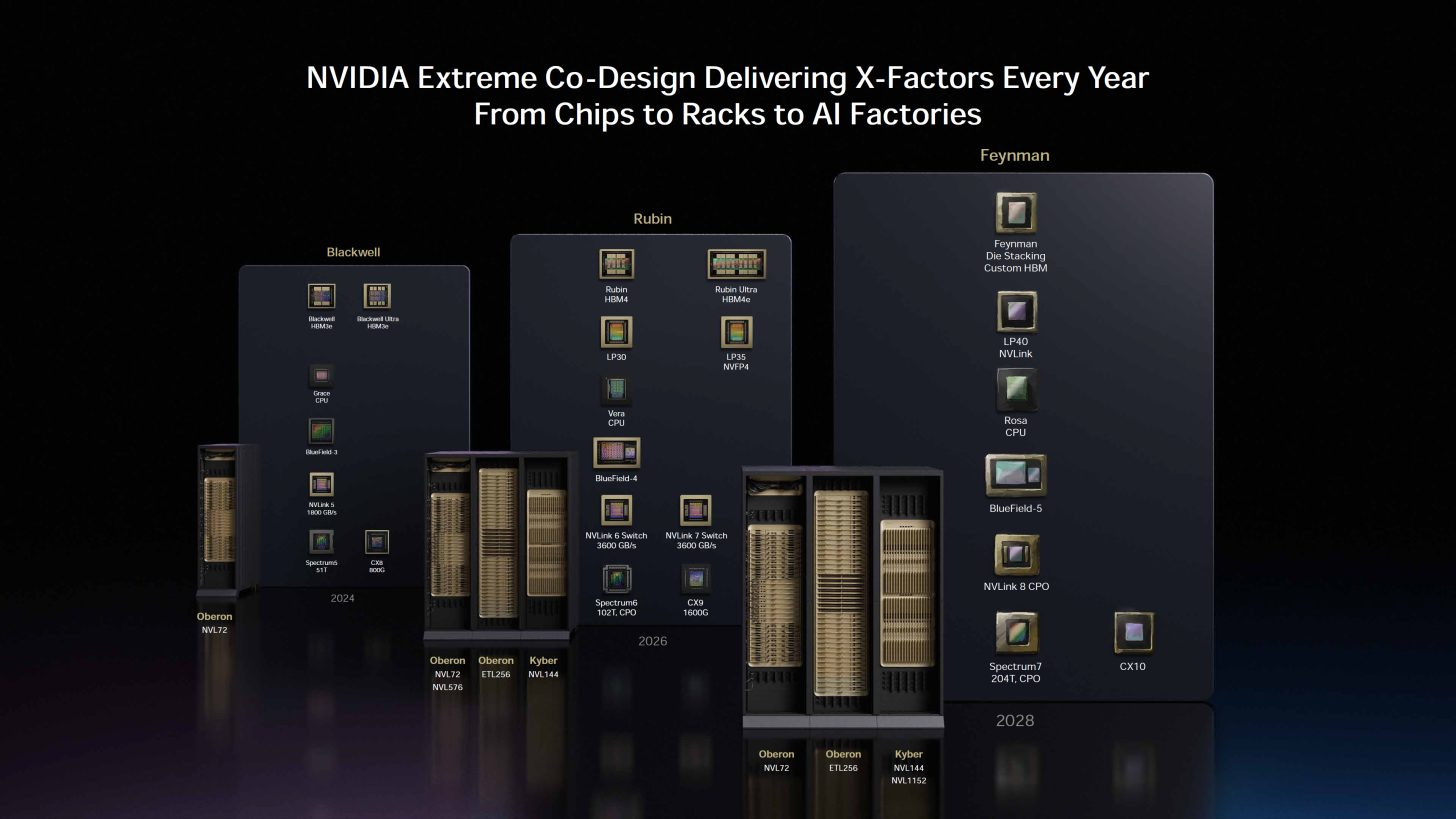

The discourse surrounding NVIDIA's future roadmap has recently entered a zone of turbulence. At the center of the storm are the ambitious plans for the next-generation Kyber server racks and Rubin Ultra accelerators. The analytical firm SemiAnalysis sparked a wave of skepticism, suggesting that the release of these solutions could be delayed until 2028. These assertions quickly permeated major financial publications, creating the illusion of a systemic crisis within the company's production chains.

The analysts' technical arguments centered on three critical points. First, questions arose regarding the midplane—the central interconnect board that, in Kyber NVL144 racks, must facilitate communication between 144 GPUs. Due to the extreme complexity of the vertical layout, it was suggested that production defect rates had reached a critical threshold. Second, reports surfaced of a forced redesign of the chip itself; according to Tom's Hardware, NVIDIA allegedly pivoted from a quad-die configuration for the Rubin Ultra to a dual-die setup, effectively halving the compute power per slot. To complete the picture, analysts pointed to a failed "Plan B"—an attempt to link two current-generation racks in a "back-to-back" configuration (NVL72x2), which cloud providers reportedly blocked due to excessive infrastructure strain.

NVIDIA's response was terse and resolute. With multi-billion dollar contracts with the world's largest data centers at stake, the company avoided engaging in detailed debate, limiting itself to a statement that its roadmap remains unchanged. This brevity acted as the ultimate stabilizer: the market reacted instantly with a surge in stock price, completely neutralizing the impact of the pessimistic reports.

For the seasoned industry observer, this situation feels like a recurring script. NVIDIA has weathered these cycles of "information attacks" before. Prior to the launch of Blackwell and Blackwell Ultra, the market was flooded with reports of thermal management issues and HBM memory compatibility problems, yet actual shipments commenced without significant delay. A similar pattern emerged with the base Rubin chips and Vera processors: following a wave of rumors regarding technical hurdles, the company simply announced the start of mass production and the first sample shipments to key clients.

It is essential to recognize that the current struggle in the AI compute segment transcends a mere comparison of specifications. Competitors such as AMD and Intel, as well as the in-house developments of Google and Amazon, are betting on TCO (Total Cost of Ownership) and energy efficiency. In reality, however, NVIDIA's dominance is sustained not only by raw silicon but by a formidable software foundation.

The CUDA and CUDA-X stacks have created an impenetrable moat around NVIDIA's hardware. Software-layer optimization allows users to extract maximum performance from the current Hopper and Blackwell generations, often neutralizing the nominal teraflop advantages of competitors. When independent tests from the MLCommons (MLPerf) consortium consistently confirm NVIDIA's leadership in the training and inference of Large Language Models, any rumors of delays become mere background noise.

Ultimately, the Rubin Ultra case reinforces a vital thesis: in the era of AI hyperscaling, real-world performance and ecosystem integration outweigh any analytical forecast. NVIDIA continues to march to its own beat, transforming every new generation of hardware into the industry standard.

The New Face of Samsung’s Wearable Intelligence

The New Face of Samsung’s Wearable Intelligence