The global PC industry has encountered its first significant downturn in two years. A critical shortage of semiconductor components—most notably memory chips—has emerged as a formidable barrier, abruptly halting a growth cycle that had spanned several quarters. Amidst mounting geopolitical instability, the market is entering a period of volatile transformation, one where securing resource access now outweighs the efficacy of marketing strategies. Brand survival and market dominance are now contingent upon the agility and efficiency of supply chain management in an era of acute resource scarcity.

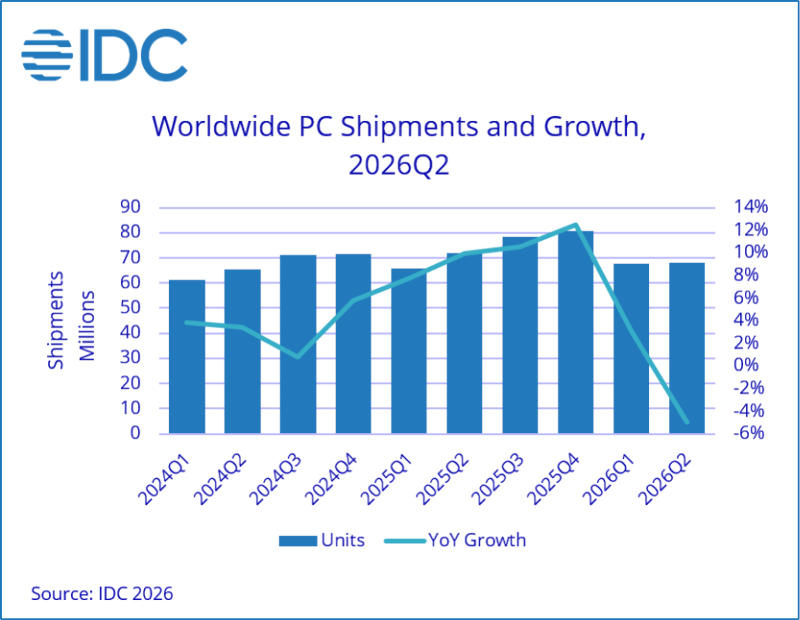

The results for the second quarter of 2026 have unveiled a troubling trend: global PC shipments contracted by 4.9%, falling to 68.2 million units. According to IDC, this marks the first decline following nine consecutive quarters of growth. The primary driver of this stagnation has been an acute shortage of RAM and NAND flash memory chips, which has forced manufacturers to pivot their strategies toward emergency stockpiling.

The situation is further exacerbated by a market caught between the geopolitical crossfire and a systemic technological deficit. Within this dynamic, a peculiar economic paradox has emerged: while physical shipment volumes are declining, aggregate manufacturer revenues continue to climb. This is the result of vendors hiking retail prices at a pace that outstrips the drop in consumer demand. Essentially, the market is shifting into a mode of "premium scarcity," where the total cost of ownership rises even as sales volumes dwindle.

The outlook for the coming years remains bleak. Analysts suggest that the memory shortage is unlikely to be fully resolved before early 2028. While another wave of aggressive stockpiling is not expected, market growth is projected to slow significantly in the second half of this year. Furthermore, the industry is bracing for another round of price increases in 2027, which could create a structural barrier to mass hardware refresh cycles.

Adding a layer of complexity to the crisis is the evolution of local artificial intelligence. The surge of interest in Edge AI—positioned as a more private and cost-effective alternative to cloud computing—demands substantial amounts of high-speed memory. However, soaring component costs may perversely stifle the PC upgrade cycle: users may be forced to cling to legacy devices long past their prime, even if those machines lack the hardware necessary to support modern neural network functions.

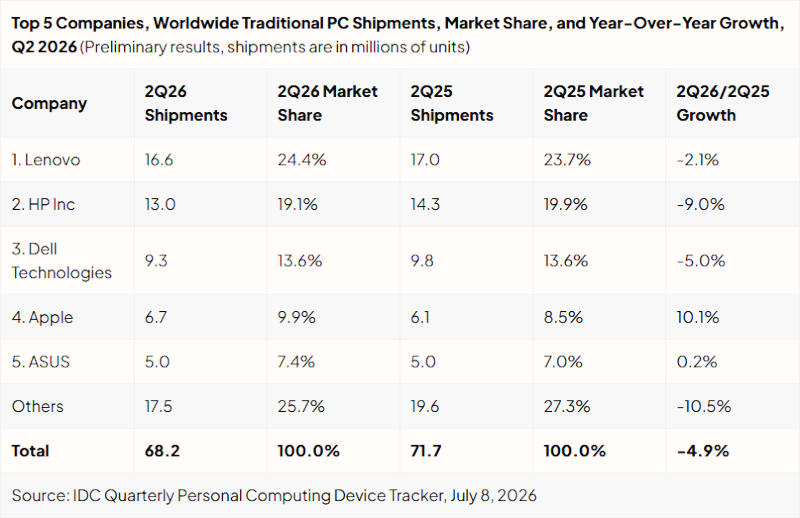

Against this backdrop, we are witnessing accelerated market consolidation. Industry titans—Apple, Dell, and Lenovo—are leveraging their immense scale and business diversification (including server solutions and smartphones) to secure priority access to critical components. This is creating an insurmountable chasm between the market leaders and smaller players, who simply lack the necessary leverage to pressure chip suppliers.

A prime illustration of this strategy is the success of Apple with the launch of the MacBook Neo. Despite the necessity of further increasing already premium price points, the company managed to solidify its market position. This reinforces the thesis that in an era of scarcity, brand loyalty and vertical integration have become the primary instruments of defense against market volatility.

The Era of Digital Recruiters in the US

The Era of Digital Recruiters in the US