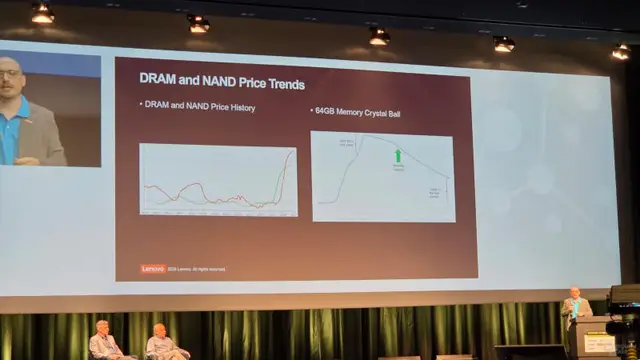

The global semiconductor market is entering a phase of structural transformation, rendering traditional memory price cycles obsolete. Driven by the rapid expansion of artificial intelligence, the current surge in demand for computational power is rewriting the playbook for both manufacturers and consumers. Lenovo warns that a return to the pricing benchmarks of previous years is unlikely; instead, transient shortages are giving way to a "new normal" that will compel the industry to fundamentally rethink its approach to server architecture.

The server infrastructure industry has collided with a stark new reality: the cost of volatile and non-volatile memory chips no longer adheres to traditional market cycles. At ISC 2026, Lenovo representatives were candid, stating that the era of cheap memory—a staple for system integrators for years—is officially over. Even with the massive expansion of production capacities planned for the coming years, the likelihood of prices returning to 2024 or 2025 levels is effectively zero.

This is not a temporary price spike, but the establishment of a new economic paradigm. Experts predict that by 2030, the market will stabilize at a high plateau, creating a "new normal." This scenario is reinforced by the strategies of industry titans like SK hynix. The Korean giant intends to triple its production capacity by 2034; however, this move is not designed to trigger a price collapse, but rather to keep pace with a colossal and relentlessly growing demand. In this new framework, the supply surpluses that once fueled price wars are now instantly absorbed by the insatiable appetite of hyperscale data centers.

As permanent deficits and high component costs become the baseline, the very philosophy of server architecture is evolving. Where over-provisioning RAM was once considered a safe standard and a benchmark of system power, such an approach is now economically unjustifiable. The industry is pivoting from brute-force capacity expansion toward intelligent memory distribution.

The defining trend is a strategic shift in focus from Central Processing Units (CPUs) to Graphics Processing Units (GPUs). Modern systems increasingly rely on specialized accelerator memory which, while still consuming system resources, does so with far greater efficiency. For instance, in a traditional dual-processor system with 32 memory slots, the minimum threshold for comfortable operation was typically 1 TB. New architectural approaches are radically redefining these figures.

A prime example of this transformation is found in Nvidia’s GB200 solutions based on NVL4. In this configuration, the total memory capacity is approximately 1 TB, but it is distributed fundamentally differently: the primary load is carried by HBM3e (High Bandwidth Memory), with 186 GB allocated to each of the four GPUs. Meanwhile, the two CPUs are allocated a mere 240 GB of LPDDR5 memory (roughly 120 GB each). For modern high-performance servers, such system memory volumes seem strikingly modest, yet this precise optimization allows the system to operate at peak efficiency without inflating the budget.

This trend of stripping away redundancy is evident across other product lines. In systems featuring Vera processors, Nvidia has halved the maximum memory capacity, reducing it from 1.5 TB to 768 GB. Such optimization yields a direct financial impact: in NVL72 rack-scale solutions, reducing SOCAMM capacity from 55 TB to 28 TB generates massive cost savings without resulting in a critical loss of performance.

Ultimately, the industry is transitioning from an era of "memory overhead" to an era of precision engineering. In a landscape where the cost of every gigabyte has become a strategic variable, the winning systems will not be those with the most memory, but those that utilize it with maximum efficiency.

The Road to Artificial General Intelligence

The Road to Artificial General Intelligence