The home networking market is mired in a prolonged slump, driven by a saturation of consumer demand. Following the pandemic-era surge, the industry has collided with a new era of consumer pragmatism and shifting ISP strategies. Declining shipment volumes suggest that even the introduction of cutting-edge technological standards is no longer enough to trigger widespread hardware refresh cycles. Consequently, the sector is now scouting for new growth levers within hyper-specialized niches, while awaiting a fundamental paradigm shift in communication protocols.

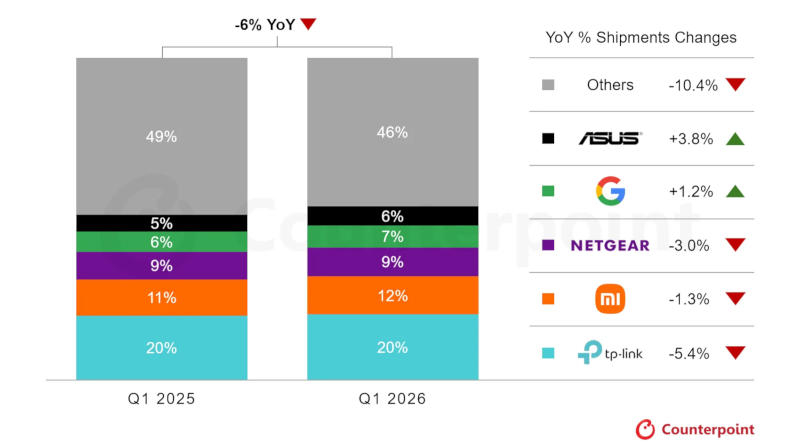

The contemporary home Wi-Fi router market has entered a phase of deep correction. By the end of the first quarter of 2026, global shipments declined by 6% year-over-year. However, this figure is merely the tip of the iceberg: from a long-term perspective, total shipments have plummeted nearly 34% from the 2021 peak, when the world was in the grip of pandemic-driven demand for remote work and digital entertainment.

Sales dynamics reveal a stark divergence among manufacturers. While most players are losing ground, Asus and Google managed to post modest growth of 3.8% and 1.2%, respectively. This resilience likely stems from the strengthening of their ecosystems and a strategic pivot toward the premium segment. Conversely, mass-market brands such as Xiaomi, Netgear, and TP-Link saw declines ranging from 1.3% to 5.4%, while smaller manufacturers are losing market share even more precipitously, with drops exceeding 10%.

The drivers behind this prolonged decline are multifaceted. First, the market is grappling with saturation; users who upgraded their hardware in 2021–2022 feel little urgency to replace their devices. Second, macroeconomic pressures have become dominant, as the rising cost of essential goods forces consumers to defer purchases of high-end electronics.

A third critical factor is the evolution of ISP business models. Internet service providers have begun offering high-quality rental or bundled equipment that sufficiently meets the needs of the average user, effectively eroding the customer base for third-party vendors. Even the introduction of the Wi-Fi 7 (802.11be) standard, with its impressive speeds, has failed to trigger a mass migration, as the real-world performance gains for typical home use remain marginal.

Nevertheless, two growth trends emerge from the general downturn. The first is the proliferation of Mesh systems. Consumers are increasingly prioritizing seamless coverage across all rooms, opting for a network of interconnected nodes over a single high-powered router. The second vector is gaming. Gaming routers are seeing sustained demand due to latency optimization and increased throughput, providing a tangible competitive edge in online gaming.

The market is expected to begin recovering in the second half of 2026 or early 2027. The primary catalyst will likely be the release of Wi-Fi 8 compatible models. Unlike previous iterations, which focused primarily on raw data throughput, the new standard will shift the emphasis toward reliability, connection stability, and efficient traffic management in high-density device environments.

The Evolutionary Trajectory of the Perfscale System

The Evolutionary Trajectory of the Perfscale System