The global electronics market is entering a phase of profound structural transformation. The global AI arms race has fundamentally realigned the priorities of semiconductor manufacturers, leaving the mobile segment grappling with acute shortages. Consequently, leading Chinese brands are being forced to radically overhaul their 2026 supply projections as they confront an unprecedented surge in costs. This crisis exposes the inherent vulnerability of the mass-market device segment when pitted against shifting technological imperatives.

The mobile device industry is grappling with a severe systemic shock. Leading Chinese players—Xiaomi, Oppo, and Vivo—have officially notified their partners of drastic reductions in shipment targets. In some instances, these downward revisions have reached 30%, signaling not merely a temporary downturn, but a profound crisis within supply chains and a rapid surge in component costs.

The dynamics surrounding Xiaomi are particularly concerning. While the company aimed for shipments of 170 million units last year, current forecasts were first moderately adjusted to 135 million, before plummeting further to 95 million units. This precipitous drop is driven by a critical shortage of components and runaway price hikes. The situation remains so volatile that the company has warned suppliers of further potential cuts should logistics and production chains fail to stabilize. A similar trend is evident with Oppo and Vivo, whose forecasts have dipped below the 90-million-unit mark, while Honor has conceded that maintaining its previous growth trajectory is no longer feasible.

For brands targeting the entry-level segment, the blow has been most acute. Rising costs for basic components are effectively eroding the margins of budget models, transforming their production into a precarious undertaking. Simultaneously, a notable shift in consumer behavior is emerging: as new devices become more expensive, users are extending the lifecycle of their current gadgets. This has triggered a surge in demand for repair services and the refurbished hardware market.

The catalyst for this collapse is a global memory chip shortage that has impacted even giants like Apple. However, the root of the problem lies deeper—in the aggressive expansion of artificial intelligence. Today, the mobile electronics sector is forced to compete for fabrication capacity with Nvidia and other AI accelerator developers. In this hierarchy of priorities, smartphone manufacturers have found themselves at the bottom of the list.

Compounding the crisis is a strategic realignment by key mobile processor developers. Qualcomm and MediaTek have begun aggressively pivoting their resources toward the data center market, where profit margins are significantly higher. MediaTek has already openly warned clients of impending price increases, which will exert further upward pressure on the final retail cost of devices.

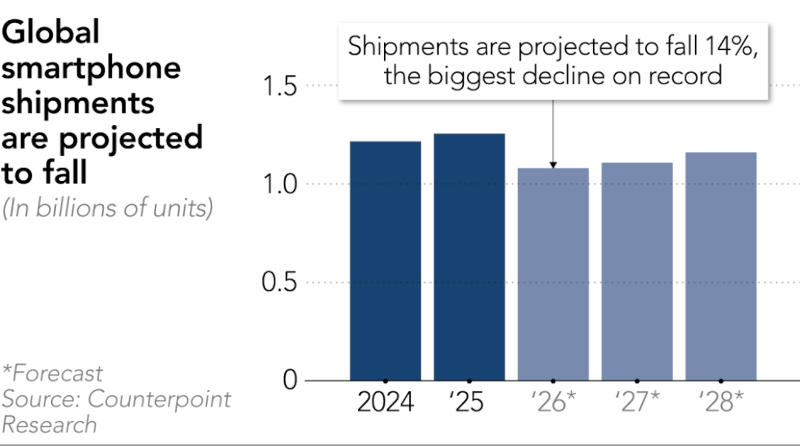

Analytical data from Counterpoint Research and IDC paint a bleak outlook: the overall smartphone market is expected to contract by 14% by 2026. The Android ecosystem, dominated by Chinese brands, could see an even steeper decline of up to 21%. Against this backdrop, Samsung appears to be a more resilient player, a position attributed to its strategic focus on the premium segment and more prioritized access to memory supplies.

The crisis extends beyond semiconductors. There is a pervasive rise in the cost of printed circuit boards (PCBs), fiberglass, and even basic chip packaging services. Consequently, the industry is entering a period of rigorous optimization, where survival will depend not on market share acquisition, but on a company's ability to manage overheads amidst total resource scarcity.

Intel’s Technological Gambit: The 14A Node

Intel’s Technological Gambit: The 14A Node