The global electric vehicle market is undergoing a tectonic shift, as years of single-player dominance give way to cutthroat competition. The rivalry between Tesla and Chinese behemoth BYD has evolved into a strategic clash between two fundamentally different philosophies of scaling. Today, success is measured not only by delivery volumes but by the agility to navigate cooling demand across the world's leading economies. At the heart of this conflict lies a pivotal question: who will be the first to architect a comprehensive ecosystem for autonomous transportation?

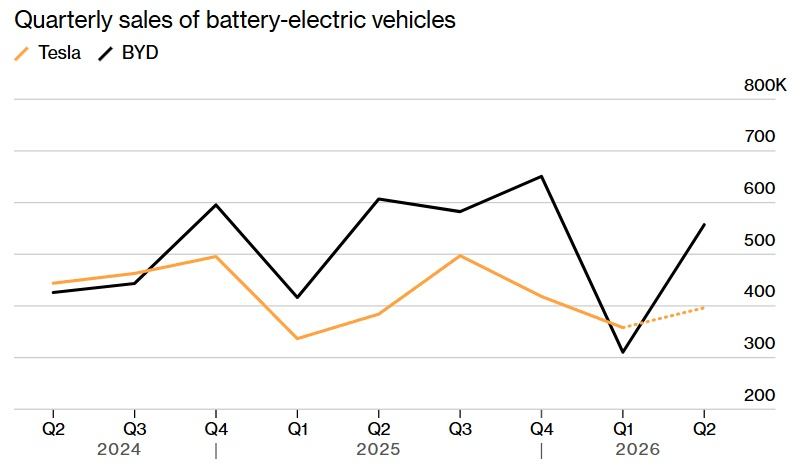

The global electric vehicle market has plunged into a period of intense volatility, with leadership shifting from quarter to quarter. Latest data confirms that BYD has reclaimed its crown: in the second quarter, the company delivered 557,090 battery-electric vehicles (BEVs). While this figure is slightly lower than the results from the same period last year, it allows the Chinese manufacturer to decisively outperform Tesla, whose deliveries for the same window stood at approximately 396,500 units.

This dynamic reflects a protracted game of leapfrog. BYD first seized the initiative in the fourth quarter of 2024, maintaining its lead throughout a significant portion of 2025. However, the first quarter of this year saw a fleeting victory for Tesla, which regained the top spot with a lead of roughly 48,000 vehicles. This temporary setback for BYD was driven by domestic headwinds in China—a sharp decline in consumer demand within the local market, which has traditionally served as the company's primary stronghold.

However, the Chinese giant's strategy has pivoted. The focus has shifted from domestic reliance toward aggressive international scaling. In June, BYD's total sales across all powertrain types grew by 5.5%, reaching 403,472 units. Notably, nearly 43% of this volume was generated in overseas markets. This geographic diversification is becoming the primary hedge against local economic crises, allowing the company to scale faster than its competitors.

Parallel to this quantitative growth, BYD is engaged in an existential technological arms race. Within China, a brutal price war has erupted, where the primary weapon is no longer mere cost reduction, but product modernization. Under pressure from ambitious players like Geely and Xiaomi, BYD has shifted its focus toward intelligent vehicle operating systems.

The primary theater of conflict has become Advanced Driver Assistance Systems (ADAS) and autonomous driving. In late May, the company unveiled a proprietary silicon chip for autonomous systems, which developers claim is the most powerful in the Chinese industry. When coupled with the accelerated production of next-generation batteries—an area where BYD maintains a traditional edge through vertical integration and its own lithium processing plants—this creates a formidable technological barrier for competitors.

Nevertheless, the broader industry outlook remains nuanced. Although global EV sales are pushing toward new records, growth rates in key markets are beginning to decelerate. In China, long the industry bellwether, a troubling trend has emerged: in May, sales of New Energy Vehicles (NEVs), including both BEVs and plug-in hybrids, fell by 7.5% compared to the previous year.

This downturn indicates that the market is transitioning from the early adoption phase into a maturity cycle, where consumers are becoming more discerning and growth is no longer automatic. In this new reality, victory will not go to the first company to launch a mass-market electric car, but to the one capable of delivering a seamless software ecosystem and a stable, global infrastructure.

Intel’s Technological Gambit: The 14A Node

Intel’s Technological Gambit: The 14A Node